Shifting Surgical Horizons and the Move to Outpatient Procedures

A surgeon performs a procedure in this studio photograph.

Getty Images

Note from the editor

More orthpedic procedures are moving to outpatient Ambulatory Care Centers as physicians say the ex-hospital facilities let them better control expenses and the patient experience, while keeping costs lower than they would be in a hospital. By owning the equipment and focusing on one specialty, it’s easier to schedule procedures and run an operating room more efficiently, and they add, professionally more fulfilling.

Across the U.S., there are now more than 6,000 ASCs, up from more than 5,000 in 2010, according to the ASC Association, a lobbying group for the facilities. Orthopedic procedures in particular have shifted to outpatient centers, driven in part by the pandemic and also by Medicare’s increased willingness to pay procedures performed at ASCs. Total knee replacements were added in 2020, and total hip replacements in 2021.

Seeing an opportunity, medical device companies are increasingly catering to ASCs, with financing plans for equipment and even teams to help construct and design surgical centers.

Medtech execs ‘rethink’ long-term strategies as care settings shift: Accenture report

By: Nick Paul Taylor• Published Nov. 10, 2022

Dive Brief:

More than 75% of surveyed medtech executives expect expanding care settings and delivery models to “significantly re-orient their company’s long-term strategy.”

The Accenture global poll of 150 senior medtech executives found that the move from hospitals to ambulatory and at-home care will require medical device companies to “completely rethink their business approach.”

In response, many firms are “simply identifying and re-labeling team members” to create digital health teams. Accenture suggests the industry will be better served by “upskilling and reskilling existing” staff while blending and incubating external talent.

Dive Insight:

The COVID-19 pandemic accelerated shifts that were already underway in the industry, notably moves from in-person to virtual interactions and from hospital to ambulatory care centers. According to Accenture’s report, which is based on the survey and interviews with 30 digital health senior executives and C-suite leaders, the shift in where care happens is only just beginning.

“We estimate that 80% to 90% of chronic and behavioral care can shift to virtual. It means that providers are able to work to the full extent of their medical training, rather than burning time on more menial tasks,” an unidentified executive at AdvaMed’s Digital Health Center of Excellence said in the report.

The surveyed and interviewed executives expect to transform their businesses in response to the shifts in how care is delivered. While traditional products still account for most sales, the executives see the expansion of care to new settings as part of their growth strategies. Accenture cited the use of diagnostic tests at physician’s offices or at home, rather than at large hospital labs, as an example of the changes.

Other parts of the survey cover the emergence of the “consumer patient,” the rise of digital, the convergence of different sectors and emergence of new regulatory pathways. Most (86%) of respondents said future success will depend on companies targeting the entire care pathway rather than specific products and services.

Article top image credit: Getty Images

Friday Q&A: GE Healthcare’s Arduini, Zodl talk about spinoff, M&A, margins, Jack Welch

The CEO and CFO of the company spoke with MedTech Dive just weeks before the healthcare business formally separates from General Electric.

By: Peter S. Green• Published Dec. 9, 2022

As GE Healthcare prepares to go public as an independent company on Jan. 4, CEO Pete Arduini and CFO Helmut Zodl joined the rest of the firm’s top management to presentthe company’s future to analysts and investors in New York City. As a standalone firm, GE Healthcare forecasts compound annual growth rates of 3% to 7% across all its business sectors, an adjusted EBIT margin as high as 20% and increasing connectivity through its Edison AI platform.

This interview has been edited for length and clarity.

MedTech Dive: What's going to be different now that you're a standalone company?

PETE ARDUINI: The focus that we will bring by having our own balance sheet. We'll be able to invest in, I'd say, more apropos healthcare investments, that's a really important part. We've been a bit more of a giver in the past few years as part of GE, so to actually be able to put more into health technology, I think that's number one. Two, and this is part of how Helmut and I run the company, is just a more agile company. Decisions can take months, and I would say, the clock speed of the company, moving it from a focus on the quarter into focusing on the week, so we're well into that process. The other side is back to our core of innovation and investing at higher levels, and how we go to market and then also our digital capabilities, which are growing quite a bit.

The current economic situation for startups, with valuations plummeting and VCs running out of cash, seems to open up an opportunity for the big players like yourself.

ARDUINI: We have a lot of work to do, just coming out as a separate company here the first week of January and executing on our organic strategies. That being said, M&A has been and always will be an important part of the strategy. Whether it be collaborations, distribution agreements or actual acquisitions, I think you're going to see, particularly in the digital area.As those values change on [the] right assets out there, we're clearly going to be looking. Some of these take years to build the relationships. In my very first week, we started a weekly M&A [meeting]. Much of that is, hey, so there's Company X, that's an interesting area, we might want to partner to do something with them, who's got the relationship? How do we start building that relationship? And now we're starting to see fruits of that activity, which started years ago.

HELMUT ZODL: For us, it’s also having those four great platforms: imaging, ultrasound, patient care solutions and pharmaceutical diagnostics. So where something can fit in really nicely, it can plug in very quickly. That's something that we're quite excited about, because leveraging those platforms, it's quite unique for a player like us.

So you would be looking at acquisitions that slot into the Edison platforms?

ARDUINI: Yes, across the board. That's an enabler. A lot of times when companies are spun out, you know, it might be the black sheep of the family. We come out with a strong balance sheet, great credit rating, great products and already a running start. And that's important because the investment started a couple of years ago. And so now we're seeing the benefit of those products. We're actually seeing our growth rates increase. We've got pathways to the margin expansion. So it's not like you know, January 1, “Hey, what are you gonna do?” There has been a build up to this moment, which is one of the reasons we’re confident in what we can do.

What would Jack Welch say about this spinoff?

ARDUINI: Jack would probably start stuttering. But look, I think from a standpoint of the company and what we're doing, I think he would be very proud of the direction GE Healthcare is going, by itself and separate. We won't be able to ask Jack that, but I think what Jack was very good about was doing the things that are going to make a difference for customers and patients. And that's really at the core of what we're doing, and I think we can do it more effectively as a separate company.

Speaking of M&A and companies that have seen a massive decline in valuation, is Philips a target?

ARDUINI: We wouldn't comment about any companies, but you know, with the combinations of what we do in the marketplace, there's so many other areas and places that we would look at to go to grow.

You’ve laid out optimistic growth targets over the next three to five years in a high interest-rate environment, with hospital systems pressured to cut spending. How do you maintain high margins?

ZODL: The margin expansion is executed in three phases, Phase one is really about how we improve our commercial execution. We talked a lot about what's happening in pricing, and how can we get more productivity at a lower cost or on a certain path. [Last year and this year], we paid a significant amount of incremental costs, because parts availability was very challenging. Some of this will go away. Logistics is another key driver in offset, which has reduced already this year. [We are also] taking substantial actions on our cost structure: we took a restructuring in the third quarter, and we will really look very carefully where we have the opportunity to reduce costs. One of the biggest jobs that has already started is [to] look at our IT infrastructure coming from a $100 billion company, GE, to an $18 billion company, GE Healthcare. We have a great opportunity to improve and lower our costs in the infrastructures we have across the company.

Then I think it's all about how we can continue to grow the company. Mid-single-digit [sales] growth to get leverage will also be important.

The third piece is to be all about innovation. If you are first to market with a new innovation, if you're the one that really is pushing the envelope, whether it's on the device or the digital side, that's really what differentiates and you can demand a higher price and you can demand higher profitability. The more we bring this forward in those four businesses, we will continue to expand our margin as we go forward.

ARDUINI: Our customers have got big patient backlogs, people waiting to get exams and studies, so we're part of the solution to actually solving that for them. And in many cases, they're paying more for labor [and many] of our products allow them to get more done in that same high-cost labor window. So when they're saying, gee, I need to prioritize my spending, we typically come to the top of the list, because we're typically an enabler, and that gives us the volume for growth, and then you tie the items that Helmut tied to it, that's how we see the profit coming through.

Trying to recover from some of the COVID-era supply chain issues, what concrete steps are you taking to change that structurally?

ZODL: So dual sourcing, which we have, or multiple sourcing, because we operate a very large supply chain footprint: we have manufacturing in the US, in Europe, in Asia. So having really local suppliers for local manufacturing that either serves the local market or gets exported, that's very important for us.

ARDUINI: [We’ve talked] about platforming. And what platforming does relative to supply chain is, if you've got one product area that's got five different platforms, you're trying to find all those distinct parts to all these different scenarios, and in a challenged supply chain environment that's tough. If you're down to one or two platforms, with different iterations on it, you're worth a lot more to a given supplier, that's an important part of our variable cost reductions. We just got a lot smarter during the COVID window, I think, from how we've had global supply chains [to] not moving stuff around the world as much and having it more local, where it's consumed.

There's been a big growth in out-of-hospital services, ambulatory surgical centers and ambulatory care facilities. How do you see that shaping up versus the traditional hospital market?

ARDUINI: I think the core hospital market for the previous reasons about demand is still strong, but their outpatient volume is booming. This is a global phenomenon. Procedures that typically wanted surgical backup, because of COVID people started actually moving them out. And now they're sticking [with that], so full new knee replacements, hips, we make all the visualization equipment for that. So I think you're going to see that over the next three to five years continue to grow.

Are there changes that you would like to see for the industry in the way that devices are regulated both here and in Europe?

ARDUINI: So I would say, honestly, the FDA and what has taken place with Dr. [Jeffrey] Shuren [the director of the FDA’s Center for Devices and Radiological Health] who runs our world, he has actually done a pretty good job of moving stuff through at a reasonable clip. What's on the rise for us of concerns is, as you bring more artificial intelligence, and machine-based learning models that actually learn meaning, tomorrow, it's actually a slightly different product than it was yesterday, the current approval process with the FDA just doesn't know how to contemplate that, let alone CMS [the Centers for Medicare and Medicaid Services]. I think the rest of it, it's been pretty reasonable. To your point on EU MDR, you know, there were a lot of changes made that everybody needs to comply with. We're in actually quite good shape.

Would you be willing to pay more for better expertise in AI?

ARDUINI: That's a possibility. In the drug world, when you get a product approved by the agency, you automatically get [CMS billing] coding with it. That doesn't happen in the device world. There shouldn't have to be a second process to go through CMS to get coding. Should there be user fees or other methods to pay for it? I think it should be looked at, because we've always been the most innovative country in the world, and we want to have the most innovative companies. I'm hoping that our regulators take some of that into consideration.

Correction: Corrects date of GE Healthcare’s debut as a public company.

Article top image credit: Peter S Green/MedTech Dive

Friday Q&A: Fujifilm’s Henry Izawa on navigating a tough hospital equipment market

The CEO of Fujifilm Healthcare Americas discusses integrating Hitachi’s diagnostic imaging business, new product launches, and how hospital budgets are changing the market for imaging.

By: Elise Reuter• Published April 7, 2023

Tight hospital budgets remain a challenge for medical equipment makers. “The market is very tough,” says Fujifilm Healthcare Americas CEO Henry Izawa, even as growing demand for MRI and CT machines as well as informatics technology, has helped the company. Fujifilm has focused on launching an array of new products since its parent company bought Hitachi Healthcare for $1.56 billion, and the two companies, which make imaging systems and technologies, merged in 2021. In an interview with MedTech Dive, Izawa talked about recent acquisitions, future products, and navigating a challenging economic environment.

This interview has been edited for length and clarity.

MEDTECH DIVE: How are you thinking about the broader macroeconomic environment going through 2023?

Henry Izawa, CEO of Fujifilm Healthcare Americas

Permission granted by Fujifilm

IZAWA: When I talk to the hospital CEOs, there's a lot of uncertainty. And just looking at the first two months for them, they continue actually to be in the red, which is very tough for them, because I think a lot of the CEOs expected to turn it around starting this calendar year.

Now, there has been significant improvement from one year ago, especially in the larger facilities. But it still remains [in the] red.So from that perspective, I think it's still going to be a rocky year. I still hope that CT, [MRI], the larger modalities, as well as informatics remain strong, which will help us. And hopefully, women's health also comes back, because we have a lot of new products and technologies that we've launched or are launching.

What are your top priorities for this year?

From a Fujifilm USA standpoint, we're really focusing on three areas. One is digital pathology, [the] second endoscopy in general and the third is evolution in MRI.

You acquired Inspirata’s digital pathology business in January. Where do you hope to take it in the future?

Fujifilm has been a market leader for 20 years in digitalization for medical imaging. Pathology currently is like where we were for radiology 20 years ago, where digitalization wasn’t there, everything was analog. And if we compare pathology today, it's glass slides that are being used. You have to be at the site to really make the [diagnosis].

What we've seen in the past 20 years is we're able to bring a lot of information to the radiologists or the physicians, even when they're located outside of the hospital. We’ve seen some of these trends in pathology in other countries. And it was just the right moment for us to capitalize on this and really promote this new trend in the United States.

Where is that adoption right now?

Outside of the United States, the U.K. has been a big adopter for digital pathology. In the United States, there are some facilities like [Vidant], for example, who is going to be an early adopter, and we have some other smaller sites that are on board. But I think it's a very new initiative for the clinicians.

What are your plans for MRI technology?

We acquired Hitachi Healthcare in 2019. In the United States, we were the first country to actually merge the two organizations together. And in the course of doing that, we've been very active in working with the R&D team, both from [the] legacy Fujifilm and [the] legacy Hitachi side, to really come out with innovative technologies.

We launched a product called Velocity, which is a high-field, open MRI at [the Radiological Society of North America] last year and we're hoping to get FDA clearance this year. [Coming] soon is another new product called Synergy. This is a wide bore 1.5 T [MRI strength is measured in Teslas, or T, representing the strength of the magnetic field a machine produces], which has a lot of AI technology from a de-noising standpoint and a lot of new potential. So we're very excited about this. For Fuji, what is most important is that we continue to launch new products every year. We've done this very successfully on the X-ray side, as well as on the informatics side [and] the endoscopy side. The MRI launches last year and this year [are] piggybacking on that philosophy.

What are your priorities with endoscopy?

In the last four years, we've launched about 20 new technologies, in the GI space, pulmonary, [and] surgery. The bulk is GI, but we also are very aggressive in trying to enhance our portfolio in surgery as well.

One exciting moment for us was that we had FDA breakthrough designation for a technology that we call Eluxeo Vision. This is the first technology in the world that allows endoscopic visualization for tissue oxidization. It's called hypoxia technology. And we can use this both for flexible as well as rigid endoscopies. From that perspective, I think we did a pretty good job in terms of really launching new products across the board and enhancing our portfolio. And because of this, I think we're becoming much more noticed in the marketplace.

In parent company Fujifilm’s most recent earnings report, it said sales of MRIs, CT systems, endoscopes and IT solutions drove revenue. Are the financial pressures on hospitals affecting placements of imaging devices?

From an imaging standpoint, the market is very tough. I look at the acute care space, and I look at the reports that consolidate all of the hospitals in the United States, [and] since January of last year, every single month, they were losing money. And a lot of our customers have made drastic changes to their operations. For example, OhioHealth laid off 630 people in one shot, which is really astonishing.

We see other hospitals just stopping service lines, getting out of the ER or pediatrics. We see a lot of rooms that are just left idle. Usually when equipment goes down, they ask for service. [Now], they don't want us to come in, they want to leave the room dead. We've never seen anything like this in the history of our business here in the United States. So it's very significant.

Henry Izawa

CEO of Fujifilm Healthcare Americas

There are areas that we're seeing that are slowing down. X-ray, for example, has slowed down significantly. Mammo[graphy] for breast screening, for example, has slowed down significantly as well. But we also saw an uptick in MRI and CT, from a market standpoint. And also informatics is very strong as well. So I think the hospitals are really choosing where to use their money.

This is changing the dynamic from a market segmentation standpoint as well. So inpatient volume obviously has gone down. Outpatient has increased almost double digit. So you can see that a lot of the volumes, especially the lower-reimbursed procedures, are being pushed into outpatient.

Are you working with some of those outpatient facilities, such as ambulatory surgery centers?

One of the benefits that we had for acquiring Hitachi is that they were very strong in outpatient. So it forced us to really look at the outpatient center, and when we had the R&D discussion, we were able to categorize the needs differently for what we need to have from an acute care standpoint and what is really needed from an outpatient standpoint. Because of the integration, we're able to pose things a little differently to really serve a bigger segment from a product development standpoint.

Article top image credit: Permission granted by Fujifilm

Companies see a future for smart implants. Doctors are waiting for proof.

Zimmer Biomet and Canary Medical are rolling out the first knee implant with an integrated sensor. But it will take time to figure out how to incorporate that data into patient care.

By: Elise Reuter• Published June 28, 2022

If a knee talks, who’s listening?

That’s the question facing orthopedic surgeons and rehab physicians as they learn to work with a new knee replacement that incorporates sensors and processors to send data about how the joint works from deep inside the patient’s body.

It’s one of a growing number of devices sending data to physicians to help them monitor their patients, including continuous glucose monitors and wearables to monitor for heart arrhythmia. With this influx of information, medtech companies are still ironing out how to make the data useful for doctors.

“This field is still very nascent,” said Jay Pandit, a cardiologist and the director of digital medicine for the Scripps Research Translational Institute in San Diego, noting that physicians simply haven’t got time to look at the raw data now flooding in from wearables — and soon from implantable devices.

Data still are far from being user-friendly, often requiring the physician to have a dedicated analyst reviewing the data on a third-party website, Pandit said. Most doctors have just seven to 10 minutes to meet with a patient, review their records and come up with a care plan, so there’s no time to analyze reams of raw data, he added.

Since the pandemic, the enthusiasm for remote patient monitoring devices has increased, but there aren’t any overarching guidelines on how to manage the data generated by these devices, Pandit said.

Still, that hasn’t curbed plans by smart-knee manufacturers.

“The talking knee is a reality,” Indiana-based Zimmer Biomet announced at the American Academy of Orthopaedic Surgeons’ conference last year. The company was presenting its new knee-implant extension with an embedded sensor just days after receiving de novo clearance from the Food and Drug Administration.

Now, Zimmer, which developed the smart knee along with California-based Canary Medical, Inc., a company that creates sensors for medical devices, has begun selling the replacement joint, called Persona IQ. It can measure a patient’s range of motion, step count, stride length, and walking distance from inside the human body. Still, physicians don’t yet know how to use this data to help patients.

“Turning it from ‘I have data on a patient,’ to ‘I can make a diagnosis for a patient,’ or ‘I can tell a patient what they need to do differently,’ it’s going to take some time,” said Matthew Hepinstall, an associate professor of orthopedic surgery at New York University’s Grossman School of Medicine, and co-director of its Center for Computer Navigation and Robotics.

Eventually, sensors will detect problems with implants, help patients adjust their gait or provide data to predict patient outcomes. Meanwhile, competitors are creating systems that use wearable sensors to track patient recovery and hinting at their own plans for sensor-embedded implants.

Bill Hunter, Canary’s founder and chief executive, said in an interview that medical technology companies are already unleashing a wave of sensor-loaded devices in other sectors.

“Having this ability for the device to provide the clinician with actual feedback from inside the body has implications in most every major medical device,” he said. “So I do believe that you will see this showing up in all kinds of different ways.”

Canary Medical designed a hollow extension to a stem that contains a battery, accelerometer, gyroscope and pedometer to track activity data.

Permission granted by Canary Medical

What can the data say?

Zimmer’s first challenge will be persuading physicians to use its Persona IQ device over traditional knee implants, Hepinstall said.

“I’m waiting for the wearable sensors to give enough data and for us to have enough experience with wearable sensors to understand how to act on that data before implanting something in one of my patients,” he said, adding that the sensor’s size means surgeons have to remove more bone when implanting a smart knee.

Still, said Hepinstall, “somebody’s got to put these devices in people for us to learn what they can do. Monitoring patients remotely in some way is a major priority.”

When new forms of data come in, it takes time to learn how to interpret and apply that information, Hepinstall added.

“Any time you get new information, types of information you didn’t get before, it’s not necessarily easy to figure out how to use that information effectively at first,” he said.

The data collected by these smart implants are similar to those tracked by wearable devices worn on the outside of the knee and connected to smartwatches. The main difference is in cost and compliance, physicians said, since about 30 percent of people stop using wearables, according to a 2016 survey by Gartner.

Taking data on a patient’s stride, gait and speed could help develop recovery curves to predict how patients will adapt to their implants, said Fred Cushner, Canary’s chief medical officer.

It also may be able to teach physicians how to reduce pain after a replacement and how best to position the replacement joint, he added. Cushner helped develop the sensors.

“You have to do studies, but everybody is inclined to believe that we'll be able to answer some of those unknown questions” once surgeons begin implanting smart knees and the data starts coming in, said Cushner, who is also an associate professor and orthopedic surgeon at the Hospital for Special Surgery in New York.

He noted that the smart knee is only cleared by the FDA to track a patient’s activity and isn’t indicated to support clinical decision making.

Data coming from inside the patient’s body also may help scientists design better knees, said Peter Sculco, also an associate professor of orthopedic surgery at the Hospital for Special Surgery.

“That is an incredible treasure trove of research,” said Sculco, who consults for Zimmer but wasn’t involved in the development of the device.

What excites him about the smart knee?

“The ability to be able to compare and contrast the different ways we put our knee replacements in, their alignment, their balance, the designs that we use, the type of plastic we use, and then to somehow look at this gait-level data and say, ok, maybe this is a better way to do a knee replacement,” he said.

Zimmer confirmed it has additional studies planned of its Persona IQ device, though it didn’t share the specifics.

Starting with the knees

Commercial pressures are rising on joint-replacement manufacturers as the procedure shifts to ambulatory surgery centers and implants are increasingly viewed as a commodity.

“They have been an area where companies have faced incremental pricing pressure every year,” said Ryan Zimmerman, an analyst at institutional brokerage BTIG. “For companies that are looking to differentiate themselves, adding a smart implant component makes a lot of sense.”

Knees are Zimmer’s largest source of revenue and the company reported knee sales rose 8% in the first quarter of this year, and 11% in 2021 from a year earlier. In a May earnings call, the company declined to comment on whether Persona IQ would be material to the growth of its knee business this year or next.

“I won't talk about the number of hospitals that have been onboarded, but it is significant,” Zimmer COO Ivan Tornos told investors. “The patient pipeline is also significant, above our expectations.”

Knees, and the implants that go into them, are also a good place to start using sensors, added Canary Medical’s Cushner.

They offer scientists more “real estate” as Canary develops a smaller version of its sensor, he added. In Zimmer’s knee, the sensor is attached to the stem, which is drilled into the patient's tibia.

Knee revenue in 2021

Company

2021 knee revenue

Zimmer Biomet

$2.65 billion

Stryker

$1.85 billion

Johnson & Johnson

$1.33 billion

Smith & Nephew

$876 million

SOURCE: Annual earnings reports

Cyborg revolution

The smart knee is part of a broader strategy by Zimmer to augment its products with its own robotics and technology, said Liane Teplitsky, the firm’s president of global robotics and technology and data solutions.

The sensors work much like pacemakers, she said.

“The information gets automatically downloaded to a base station that the patient has in their home, and [is] then uploaded to the cloud,” Teplitsky said.

Surgeons can use HoloLens smart glasses (made by Microsoft) to guide themselves through instrument assembly, and during surgery to implant the knee, Zimmer’s surgical robots assist and collect data.

The smart knee connects to an iPhone application called Mymobility, which can pull in kinematic data from the implant and a patient’s Apple Watch to track exercise after surgery.

“Everything that we're thinking about now bringing to the marketplace will either generate data or collect data,” Teplitsky said. Eventually, Zimmer will be using sensors in more of its implants, including cementless knees and shoulders. Canary Medical already has patented sensors for heart valves, spinal implants and stent grafts.

Zimmer also has used data from the Mymobility app to power a feature called WalkAI intended to predict which patients may have a slower gait 90 days after hip or knee surgery. The company will need clearance from the FDA to use the data to make care recommendations.

“You can go from being able to predict to then being able to recommend,” Teplitsky said. “That's still the future. We can make no claims around that yet today, but that's ultimately the goal.”

A view of the physician dashboard for Zimmer Biomet's Mymobility system.

Permission granted by Zimmer Biomet

Other companies look to sensors

Zimmer’s competitors have yet to introduce their own smart knee implants, but they are betting on the need for data, largely through wearables.

Stryker, the second largest maker of knee implants by revenue, last year acquired OrthoSensor, whose technology is incorporated in knee implants to help surgeons balance the knee during surgery. Zimmer and Smith & Nephew, the fourth-largest kneemaker, have used OrthoSensor’s technology in their knee-replacement systems.

Stryker also uses OrthoSensor’s wearable sensors, which are attached above and below a patient’s knee, to track their range of motion, gait and other information before and after a procedure.

“It's all about information that the surgeon is able to use for each and every unique patient that's out there. And its application is definitely for both pre-surgery to get some baseline type information for a shorter period of time, and then up to 90 days after surgery, so that you can really see progress,” said Don Payerle, Stryker’s president of joint replacement.

Stryker likely will begin adding sensors to implanted products as well, said Richard Newitter, an analyst with financial services firm Truist.

Johnson & Johnson also is working on smart implants, according to Shagun Singh, an analyst with RBC Capital Markets.

“They said they own over 50% share of the trauma market. And so they want to go to that market first,” Singh said.

Looking to the future

The technology may be nascent, but sensors that will allow patients and physicians to monitor their health and improve outcomes have become an “area of important focus and development” for the medical device industry, said Truist’s Newitter.

“It’s not just about the actual implant itself anymore — it’s about building an entire digital ecosystem around the care continuum for surgery,” Newitter said.

To be sure, sensors come at a cost. Zimmer prices its sensor-equipped implants at $1,000 more than those without sensors, notes RBC’s Singh.

It likely will be a few more years before there’s enough data to show the sensors can improve health outcomes and lower costs for insurers, according to Newitter.

“We’re interested to see if it takes off, similar to robotics,” said Zimmerman of BTIG. If it does, “you should see a lot of the other companies follow suit,” Zimmerman added.

Article top image credit: Permission granted by Zimmer Biomet

Joint replacement business likely to be busy for the next year or more: BTIG analysts

By: Nick Paul Taylor• Published March 14, 2023

Dive Brief:

The outlook for orthopedic procedures “appears far more favorable” than one year ago and will support growth in the coming quarters, according to analysts at BTIG.

After talking to medtech companies at the American Academy of Orthopaedic Surgeons (AAOS) meeting, the analysts said they expect improvements in staffing and a backlog of patients to translate into “robust knee and hip growth for at least the next 4 to 6 quarters.”

The analysts continue to favor Stryker over Zimmer Biomet, although they think the latter company will benefit from improving patient volumes and the launch of its cementless knee.

Dive Insight:

One year ago, inflationary pressures and supply chain problems dominated discussions at AAOS. This year, inflation remains high and some supply chain problems persist, but the analysts found companies were singing “a far different tune,” encouraged by a procedure outlook that appears more favorable. Attendance at the event returned to levels last seen in 2019.

The BTIG analysts expect the backlog of patients that built up in recent years to support growth of hip and knee devices for 12 months or more. On a constant currency basis, Stryker’s hip and knee divisions achieved double-digit growth last year, and the analysts expect that trajectory to continue.

Management at Stryker told the analysts that many older and sicker patients are coming back into the system, and while healthcare staffing is still an issue, it is being handled better than in the past. In addition to Zimmer, Stryker competes with Johnson & Johnson and Smith & Nephew for the knee and hip markets.

Stryker, which debuted version 2.0 of its Mako robot at the event, remains the analysts’ favored firm in the orthopedic sector but they also expect Zimmer to benefit from the improved procedure outlook. Zimmer received 510(k) clearance for its Persona OsseoTi Keel Tibia late last year, addressing the lack of a cementless knee that hurt its competitiveness.

Talking to the analysts, Zimmer management forecast a 10% to 15% lift in average selling price from the cementless device. Today, the cementless product accounts for 12% to 14% of knee procedures done using Zimmer devices, the analysts wrote, and management plans to grow that figure to 20% to 30%. As the analysts note, Zimmer is “still well below [Stryker’s] cementless share of wallet."

Article top image credit: Getty Images

Zimmer Biomet gets FDA clearance for Identity shoulder system

Ivan Tornos, the company’s chief operating officer, said in August that it would be Zimmer’s biggest shoulder launch in five years.

By: Elise Reuter• Published Sept. 20, 2022

Zimmer Biomet announced Tuesday that it received 510(k) clearance from the Food and Drug Administration for a new shoulder replacement system that the company says will help surgeons tailor their approach to an individual patient’s anatomy.

The company’s Identity Shoulder System was designed to help surgeons restore rotation and a patient’s range of motion after reverse shoulder replacements, where a surgeon attaches a plastic socket to the upper arm bone and an artificial ball to the shoulder blade.

“Shoulder specialists will value this system's adaptability and flexibility to support their unique surgical approaches and complement diverse patient anatomies," Dr. William Levine, chair of the Department of Orthopedic Surgery at Columbia University who helped develop the device, said in the press release.

The system provides eight humeral tray combinations that give surgeons more options for aligning the humerus with the shoulder socket without lengthening the arm. The device was also designed to allow adaptability in the event of future shoulder surgeries, by allowing 5 mm of additional joint space below resection.

The launch is expected to be a significant one for the company, with Zimmer’s Chief Operating Officer Ivan Tornos saying in an Aug. 2 earnings call that it would be the company’s “biggest shoulder launch in the last five years.”

“This is going to be a much more customizable shoulder for a more personalized feel for the patient that should optimize movement in the shoulder,” CEO Bryan Hanson said during the call.

Zimmer Biomet’s sports medicine, extremities and trauma segment, which includes shoulder replacements, had sales of $446.4 million last quarter, a 3.4% decrease from the prior-year period.

In an emailed statement, the company said it expects to make the shoulder system available in the U.S. in the fourth quarter.

Article top image credit: Permission granted by Zimmer Biomet

Hospitals expect procedures, capital equipment budgets to grow next year: survey

By: Elise Reuter• Published March 27, 2023

Dive Brief:

Hospitals continue to face staffing shortages and financial constraints, but the majority expect the situation to improve next year, according to a survey of 40 executives and purchasing directors at hospitals by BTIG.

Three-fourths of hospitals said procedure volumes are still being affected by staffing shortages, but more than half expect to return to full capacity in 2024.

Half of the hospitals said their 2022 revenues were the same or lower than pre-COVID levels. But two-thirds expect revenues to increase this year, and most hospital executives plan to increase their capital equipment budgets in 2023 and 2024, the survey found.

Dive Insight:

Hospitals have been taking a close look at their budgets as staffing and supply costs rise, which can affect large purchases of medical equipment.

As a result, most hospitals continue to ask device vendors for price reductions and payment flexibility, BTIG analysts found in their survey. What this means for medical device manufacturers depends on the company.

Stryker, which makes orthopedic and neurotechnology devices, said in January that orders of its products had not been affected. The company reported double-digit sales growth in its medical, endoscopy and instruments divisions, and reported record installations of its Mako surgical robot in the fourth quarter of 2022.

“We are not seeing any cancellation of orders,” CFO Glenn Boehnlein said in a January earnings call, adding that because most of Stryker’s equipment produces revenue for hospitals, “you wouldn’t expect any kind of slowdown.”

Intuitive Surgical, whose da Vinci robot is used for colorectal, gynecological, urology, heart and general surgeries, said placement of its robots decreased in the fourth quarter of 2022 compared to the prior year. CFO Jamie Samath, during a January earnings call, said this reflects “cautious capital spending” by customers given the current macroeconomic environment, but added that da Vinci remains “a relatively high priority” in their capital budgets.

Some types of procedures are running at full capacity, including colonoscopies, endoscopies, cath lab procedures, and orthopedic, cardiac and spine procedures, according to the survey. Volumes are still lagging for general surgeries, elective procedures, and plastic, cosmetic and bariatric surgeries.

Hospitals said that facilities, IT and software products, and surgical equipment were their top capital spending priorities for 2023 and 2024, which could be good for “large, diversified” medtech companies including Boston Scientific, Stryker and Medtronic, the BTIG analysts wrote in a Monday research note.

“Spending on cath lab equipment is expected to become more important this year, a plus for companies focused on interventional, structural heart, and possibly electrophysiology procedures,” they added.

Testing, patient monitoring and telemedicine equipment were less of a priority in 2023, which could have implications for companies including Hologic and Masimo, the analysts said.

There is one silver lining: of the 30 executives who said their hospitals were being affected by staffing shortages, all of them expect procedures to return to full capacity by 2025.

Article top image credit: Getty Images

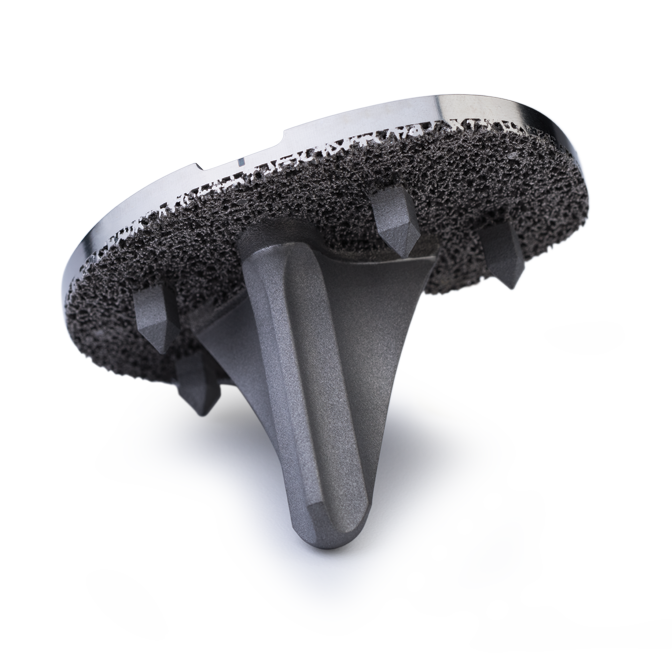

Zimmer lands 510(k) clearance for 3D-printed cementless knee replacement

By: Nick Paul Taylor• Published Nov. 22, 2022

Dive Brief:

Zimmer Biomet received 510(k) clearance for its Persona OsseoTi Keel Tibia for cementless knee replacement.

The Food and Drug Administration clearance covers a porous version of the Persona anatomic tibia. Zimmer has paired the tibia with technology that uses anatomical data in combination with 3D printing to try to directly mimic the architecture of human spongy bone.

Securing the clearance gives Zimmer another potential growth driver as the company seeks to build on the 2% increase in knee-joint sales it recorded in the third quarter.

Dive Insight:

Cementless knees have transformed the U.S. orthopedic market in recent years, leaving companies that lack the technology, such as Smith & Nephew, scrambling to add the devices to their portfolios. Zimmer has been building out its cementless portfolio for years, securing FDA clearance for the Persona Trabecular Metal Tibia in 2018 and now adding a 3D-printed product to its arsenal.

Zimmer is pitching its latest product as having optimized fixation, rotation and stability. Using anatomical data, the medtech company has sought to reduce micromotion and improve bone coverage. The porous OsseoTi technology is designed for biological fixation.

Optional Caption

Courtesy of Zimmer Biomet

While the product works in cementless procedures, it also enables surgeons to switch to a cemented approach up until final implantation using a single instrument tray. Ivan Tornos, chief operating officer at Zimmer, outlined the perceived benefits of giving surgeons the option to perform cementless and cemented procedures.

“Adding the Persona OsseoTi Keel Tibia to our well-established and clinically proven Persona Knee System allows surgeons to better address the needs of their patients with a comprehensive single system solution for a cementless or cemented application,” Tornos said in a statement on Zimmer’s website.

The bone preparation is the same for the cementless and cemented procedures, freeing surgeons to pick their preferred approach during the operation based on bone quality and the needs of their patient.

Article top image credit: Getty Images

Medtech companies shift strategy as more orthopedic procedures move to ambulatory surgical centers

Medical device companies are offering financing plans and even design teams as more physicians open ASCs.

By: Elise Reuter• Published Oct. 5, 2022

A year ago, Dr. Brian Gruber opened Integrated Surgical Services in Phoenix, transforming a former grocery store into an ambulatory surgical center (ASC) for outpatient orthopedic surgeries.

“The genesis of the whole thing was the ability to control patient experience,” Gruber said. “Hospitals are our friends, but there's only so far your voice can go at some of the bigger facilities.”

Physicians say ASCs give them the ability to better control expenses and the patient experience, while keeping costs lower than they would be in a hospital. By owning the equipment and focusing on one specialty, it’s easier to schedule procedures and run an operating room more efficiently, and they add, professionally more fulfilling.

“The flexibility of having your own space, your own ASC, from a surgical standpoint, it's awesome. We really like to be able to just do stuff,” Gruber said. “You don't have to go through a zillion people, all the red tape. You just do it. And if you need to cut somebody a deal financially, you do it. Just to have that ability and the power to do that, it’s liberating, really.”

Gruber is one of hundreds of physicians who have opened an ASC in the last decade. Across the U.S., there are now more than 6,000 ASCs, up from more than 5,000 in 2010, according to the ASC Association, a lobbying group for the facilities. Orthopedic procedures in particular have shifted to outpatient centers, driven in part by the pandemic and also by Medicare’s increased willingness to pay procedures performed at ASCs. Total knee replacements were added in 2020, and total hip replacements in 2021.

Seeing an opportunity, medical device companies are increasingly catering to ASCs, with financing plans for equipment and even teams to help construct and design surgical centers. For larger, pricier devices, such as surgical robots, more companies have started offering per-procedure prices, leases, and payment plans.

While many hospitals have well-established budgets for purchasing capital equipment, ASCs may look for more flexible financing options, Zimmer Biomet Chief Operating Officer Ivan Tornos wrote in an email.

“Many look for cashless options to obtain capital equipment and services along with implant and disposable purchases to offset extensive costs required for future new builds, resulting in improved operational cash flow/preserved lines of credit as they ramp procedures,” Tornos said.

Medicare payments to ASCs increased until the pandemic

Amount in billions, 2014 through 2020.

Manufacturers of orthopedic devices expect the number of procedures done in ASCs to rise, but that doesn’t mean the total number of surgeries is increasing — they’re just moving to a different setting, said Shagun Singh, an analyst with RBC Capital Markets.

“It remains to be seen if it would allow more people into the funnel,” Signh wrote in an email. “[Reconstruction] is a mature market, growing 3-4% in a normalized environment. There may be less room for market expansion vs. in other under-penetrated medical device sub-markets.”

Still, the switch has prompted medical device companies to build dedicated teams to work with ASCs.

Johnson & Johnson subsidiary DePuy Synthes, which estimates that 21% of orthopedic procedures are being done in ASCs, has an ASC team to offer custom solutions to surgeon-entrepreneurs and ASC administrators, said Andrie Leday III, the company’s U.S. commercial vice president of ambulatory surgery centers. DePuy’s assistance includes capital programs for buying equipment and help with coding and insurance reimbursement.

“While this trend was well underway for both clinical and economic reasons, COVID-19 helped to accelerate this shift,” Leday wrote in an email.

Stryker, the largest orthopedics company by revenue, estimates that 10% of joint replacements are being done in ASCs and expects that number to double in the next five years.

Hundreds of ASCs are being built every year, Chad Evans, Stryker’s general manager of ASC and neurotechnology sales, wrote in an email. The company can help with the initial planning, design and construction of new ASCs — from the waiting room furniture to implants, stretchers and other pieces of equipment.

While competitors like J&J and Smith & Nephew have dedicated teams working with ASCs, Stryker is “over indexed” in that market compared to its peers, according to Singh.

“They are actually years ahead of a lot of folks because they actually have architects,” she said. “They can have an architect, they'll build out a whole OR for you, the whole ASC setup. And then they're going to sell you everything.”

Knee and hip replacements are the fastest-growing orthopedic procedures for ASCs

Percent change in procedures performed at ambulatory surgery centers between 2019 and 2021.

Proponents of ASCs say they can perform surgeries at a lower cost with similar outcomes because they don’t have to cover the overhead costs of running a hospital. According to the ASC Association, Medicare pays ASCs 55% of the amount it pays a hospital for the same outpatient surgical procedure. For a total knee replacement, Medicare will pay an ASC $8,222, compared with $12,088 to a hospital outpatient department, according to Medicare’s price lookup tool. Still, patients pay more for the surgery at ASCs because for high-cost procedures, Medicare caps co-pays at hospital outpatient departments but not at ASCs.

In 2021, ASCs performed 16.5% of knee replacements and 12.1% of hip replacements in the U.S., according to data from Definitive Healthcare, a healthcare data firm. While Medicare now covers the two procedures at ASCs, the group has been lobbying the Centers for Medicare and Medicaid Services to add shoulder and ankle reconstruction as well as lumbar spine fusion in surgery centers.

Despite the difference in reimbursement, ASCs often spend the same amount for implants and devices as hospitals, the ASC Association wrote in a Sept. 13 letter to the CMS. In fact, hospitals are more likely to buy in bulk through larger purchasing agreements and be offered lower prices. To offset the costs, physician owners seek funding or look to strike deals with device companies.

Hospital outpatient departments still lead in most orthopedic procedures

Percent of procedures by care setting in 2021.

Partnerships to procure equipment

Gruber worked with Stryker when he built his ASC. Through a joint venture with the company, which provided capital in exchange for a promise of spending over a five-year period, he was able to procure some of the bigger equipment for the facility, such as the Mako surgical robot used for joint replacement surgery. Other large equipment, such as ultrasounds and C-arms, are typically financed.

While some physicians may choose to mix and match equipment, Gruber chose to purchase all of his from Stryker, he said.

“For me, Stryker holds the biggest service lines. They have got so much equipment,” Gruber added. “It was the ‘easy button’ to partner with Stryker in that regard.”

In many cases, physicians band together and seek financing from private equity firms to help cover the cost of opening a new facility. They can also seek joint ventures with hospital groups, like Tenet, which has spent billions to build out its ambulatory surgery unit.

New Mexico Surgery Center Orthopaedics, an Albuquerque-based ASC, opened in 2000 through a partnership between physician group New Mexico Orthopaedics and Ortholink, which helped with financing and had a management contract. Now, a local hospital also holds a minority stake in the facility, although the physician group still has the largest share, said Dr. Bill Ritchie, an orthopedic surgeon with the group.

The ASC has favored Zimmer Biomet products because of its focus on total joints, Ritchie said. Otherwise, it procures products from a mix of vendors, seeking volume discounts for items including lighting, cameras, power systems and disposable items such as drill bits. For surgical robots, the company went with “one manufacturer that we do the most business with,” and the contract is written as a lease where the cost is brought down by increasing volume.

Integrated Surgical Services decided to work with one medical device manufacturer, Stryker, to outfit most of the equipment for its operating rooms.

Permission granted by Stryker

Bartering with scale

Volume purchases are key to the success of larger groups that operate hundreds of ASC facilities. At Surgical Care Affiliates (SCA Health), a 320-facility outpatient surgery company owned by Eden Prairie, Minn.-based insurer Optum, the number of joint replacements performed each year has almost doubled from 2019 to 2022, said Amanda Conroy, who leads the company’s total joint replacement and spine service lines.

That lets SCA set the prices it pays device vendors for total joint replacements.

“This was the first time in our company’s history that we’ve been able to collectively do that. It’s generated millions of dollars of savings for our patients,” Conroy said. Lower costs also benefit the insurance company that owns SCA.

Without the capital that a hospital can muster, SCA has used what Conroy calls “creative solutions” to obtain expensive equipment, including surgical robots, specialty operating tables and imaging equipment. It decides on a case-by-case basis whether it's more cost-effective to purchase equipment or lease it.

Partnering with equipment vendors is key, said Brandon Hollis, regional vice president of musculoskeletal operations for Amsurg, which has more than 250 ASCs across the U.S.

“A capital purchase would be a much more simple process for a hospital system whereas now in the ASC industry, what we see with a lot of the larger, more expensive pieces of equipment, including robots, x-rays and microscopes… the vendors have done a really good job of offering different types of payments plans,” he said.

What it means for device companies

The shift from purchasing expensive equipment outright to renting or financing has shown up in device makers’ quarterly earnings.

Both Stryker and Zimmer Biomet, which is the third largest in orthopedics, said the shift has resulted in less upfront revenue from their surgical robots, which help surgeons with knee and hip implant placement.

Stryker reported that sales of its Mako surgical robots climbed 19% in the second quarter of 2022 compared with the year-earlier period, although the deal mix resulted in less revenue per quarter. The company also said the ratio of sales of its Mako robots at ASCs versus hospitals gradually has been increasing.

“This has been happening over the past kind of six months where we are seeing more deals being financed versus outright purchased, and actually a move towards more rental agreements,” CEO Kevin Lobo said in an Aug. 2 earnings call.

For its part, Zimmer Biomet has said about 30% of installations of its ROSA robots have been in ASCs.

Although the amount medical device companies currently get is the same no matter the setting, that could change in the future, according to RBC Capital’s Singh.

“The ASC is a lower cost setting and reimbursement is also lower. So at some point, I do expect some pricing headwinds for the ASC setting, which may impact our medical device companies, but we have not seen it yet,” Singh said.

Article top image credit: Permission granted by Stryker

Shifting surgical horizons & the move to outpatient procedures

Across the U.S., there are now more than 6,000 ambulatory surgery centers (ASCs), up from more than 5,000 in 2010. Seeing an opportunity, medical device companies are increasingly catering to ASCs with financing plans for equipment and even teams to help construct and design surgical centers.

included in this trendline

Medtech execs ‘rethink’ long-term strategies as care settings shift

Companies see a future for smart implants. Doctors are waiting for proof.

Hospitals expect procedures, capital equipment budgets to grow next year: survey

Our Trendlines go deep on the biggest trends. These special reports, produced by our team of award-winning journalists, help business leaders understand how their industries are changing.